Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

Do you think the market hit its low? Then it is the time to step back and reconsider.

September 8, 2016

The term “falling knife” is a common expression among traders. It denotes a stock valuation or futures contract that has experienced significant decline in value. Timing markets is always challenging (i.e. impossible) – but it’s especially hard to call the bottom. Thus, jumping in at the perceived bottom with hopes to profit can prove risky – there’s always potential for more downside. Hence, that practice invokes the reference to catching a falling knife.

Traders who found themselves jumping into the fed market a month ago based on their expectations of a bottom are now feeling the pain of that decision. As noted last month, the market was poised “…for a breakout to new price levels or also potentially test new lows.” August’s market action brought the latter – the falling knife of new lows.

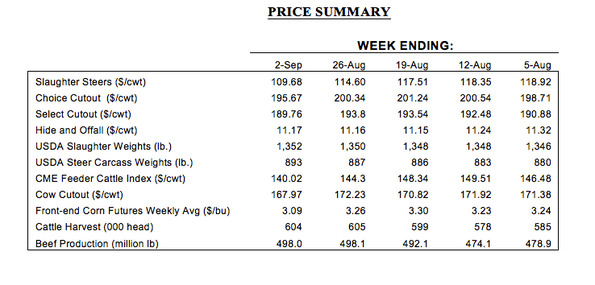

For some perspective, fed trade ended July with mostly sideways trade for the month at $117 – right in line with the monthly average, albeit that average was $6 off from June and $12 lower versus May. And given that $117 trade, there was some hope that perhaps mid-July’s $114-115 was the seasonal low.

That sentiment found some confirmation during the first half of August with trade hovering around $118-119. But then the market ran into trouble. First, fed cattle gave up another couple of dollars and retested July’s $114-115 low. And upon that retest, the market needed to hold.

No such luck. The last week of August turned especially ugly. Cattle feeders not only sold cattle early in the week, but did so around $110. Fed prices haven’t traded at that level since 2011 (Figure 1).

Simultaneously, the CME contracts also got beat up. October Live Cattle gave up $5 going into Labor Day. But more importantly, the contract finished the week by establishing a new contract low at $101.38 and barely managed to close above that low at $101.60. Worse yet, follow-through on Monday just piled on – October retreated even further, including an intra-day break below $100.

Penetration of key support levels now leaves the contract vulnerable from a technical perspective (Figure 2). Moreover, Steve Kay, writing in Cattle Buyers Weekly, points out that, “October’s deep discount to cash suggests that cash prices could go lower in September or even in October unless futures prices rally sharply, say analysts. That would depend on beef demand improving and continued slaughter levels large enough to take cattle off the market in a timely fashion, they say.”�

So, the market now heads into the fall needing to establish some semblance of positive action. The only catalyst for that to occur will be pull from the wholesale market. It’s been an especially hot summer and beef sales have struggled. The Choice cutout has largely traded around $200 since mid-July. However, pre-Labor Day sales were disappointing with Friday’s spot sales closer to $190. Cooler weather and fall featuring should help to encourage inventory clearance and provide a lift to boxed beef prices.

However, on the other side of the price equation comes consideration of fed cattle supplies. Cattle feeders have been fairly aggressive in purchasing replacements in late spring and through the summer. Placements in March, April, May, June and July have run ahead of last year by 5%, 7%, 10%, 3% and 2%, respectively. Those bigger placements represent an additional 438,000 head versus 2015 that began hitting the pipeline in August and will need to be marketed in the coming months (Figure 3).

Feedyard managers will need to be active marketers in the months to come. But the temptation is to fight the market and get bogged down with inventory – especially when the closeouts are persistently negative (Figure 4). Note that Kansas State’s data represents a cash-to-cash calculation and not intended to represent all operations, nor account for hedging coverage. Nevertheless, it’s the trend that matters and it’s relentless; over the course of 18 months (February 2015 through July 2016) the average hovers around $230 per head.

Meanwhile, as noted last month, it’s not just the beef sector that’s proving productive. Protein supplies remain ample. Pork and poultry are bringing bigger production numbers to the market, too.

To that end, last month’s column included some analysis from the Livestock Marketing Information Center: “For the first six months of 2016, U.S. beef production was 5.2% above 2015’s. At 12.1 billion pounds, that was the largest tonnage for January-June since 2013.”

Accordingly, Figure 5 represents monthly changes in meat production versus 2015. The additional total, versus 2015, is 1.273 billion pounds; 600.2, 105.7, and 567.3 million pounds for beef, pork and poultry, respectively. That’s roughly equivalent to 4 pounds of additional protein per capita in the U.S.

There’s work ahead. Undoubtedly, much of this feels like a repeat of 2015. In fact, the year-over-year chart patterns are strikingly parallel. It’s a stark reminder that markets can be brutal and unforgiving.

One thing’s for sure—we’re likely to see continued pressure and uncertainty. With that in mind, producers need to remain vigilant, disciplined and objective. Comprehensive review of operational priorities and risk tolerance will help navigate market challenges and ensure successful decision making along the way.

Nevil Speer is based in Bowling Green, Ky., and serves as vice president of U.S. operations for AgriClear, Inc. – a wholly-owned subsidiary of TMX Group Limited. The views and opinions of the author expressed herein do not necessarily state or reflect those of the TMX Group Limited and Natural Gas Exchange Inc.

You might also like:

Are you the best ranch manager you can be?

60+ stunning photos that showcase ranch work ethics

You May Also Like

Enter a zip code to see the weather conditions for a different location.