Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

Despite being volatile and choppy, the May cattle market showed some renewed strength as the wholesale trade picked up steam. But will it last?

June 8, 2016

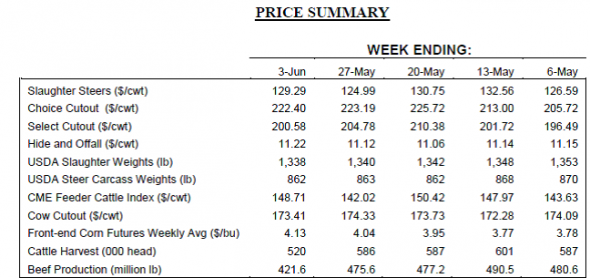

Following April, any upside seems like a victory. And thankfully, May brought some renewed strength to the market. While the month was somewhat volatile and choppy, fed cattle traded back above $130 by the middle of the month.

That occurred despite a futures market refusing to budge from the low $120s. That reality has to drag, tug and eventually challenge the market. The test occurred in the middle of the month with fed cattle trading back to the mid $120s – steady with April’s ending values. Heading into June, though, cattle feeders held strong and managed to garner better money – weigh-ups in the week following Memorial Day surged to $128-130. The market’s four-week average now stands at $129.40 (Figure 1).

The market’s resurgence in May is directly attributable to better wholesale values. The Choice cutout trumped the CME drag, jumping up to $225 in May pulling fed cattle along the way. And boxed beef values remained surprisingly steady following Memorial Day with Choice cuts indexing only about $1 lower for the week at $222.50 (and the Choice-Select spread rising to over $21 following Memorial Day – the highest level since late-2003 – another discussion for another day).

Aside from the market itself, perhaps the most significant and encouraging development in the beef complex in May (and April preceding) is tied to the volume of business that’s occurring. During the past eight weeks, cattle slaughter has totaled 4.62 million head – over 5% ahead of the same period last year. Meanwhile, beef production equals 3.76 billion pounds – nearly a 6% increase on a year-over-year basis.

Better throughput was certainly evidenced by May’s Cattle-on-Feed report. USDA indicated that April marketings totaled 1.66 million head – 1% better than last year and the third consecutive month of active selling versus 2015. From that standpoint, feedyards have been able to clean up some of the front-end and become more current. The 120-day plus on-feed inventory declined going into May with cattle feeders holding 225,000 less cattle in the category versus this time last year (placements are another story – more on that later).

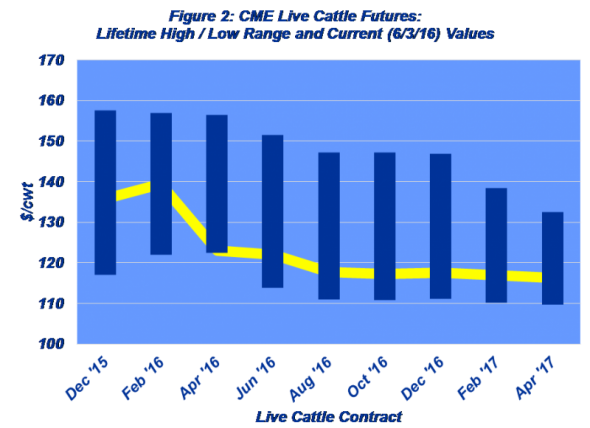

Meanwhile, packers are glad to have the cattle coming through their doors. Packer margins have been solidly positive since late-March /early-April, with the exception of the middle of May when cattle traded back up to $132. Meanwhile, cattle feeders are staring down the tunnel of a lower deferred market and trying to advance sales ahead of softer prices indicated by the futures market (Figure 2).

All of the above is mostly good news: stronger cash prices and bigger volume. However, the other side of the coin of the Cattle-on-Feed report came in the form of placements, resulting in initial bearish reaction among traders towards the deferred contracts. April placements were surprisingly large:1.66 million head – 7% ahead of 2015 and 2% bigger than the five-year average.

Confounding bigger placements was the general weight mix. There were 715,000 head of cattle over 800 pounds placed on feed during April – a record large number for April within the category. Moreover, the 800 plus pound category represented nearly 43% of the total placement mix – a new overall record, barely surpassing last September’s record of 42.76%. From a broader perspective, the 12-month moving average continues to trend upward and now stands at nearly 37% (for more detail, see Heavy-In-Heavy-Out).

Last month’s column noted that, “…feeder cattle have been pummeled along the way. Cattle feeders are fighting to get some equity back…CME’s Feeder Cattle Index finished the month below $145/cwt…off nearly $550 per head on a year-over-year comparison.” Meanwhile, this week’s Industry-At-A-Glance provides a somewhat different perspective on feeder prices thus far in 2016.

That is, the market adjustment is all relative. Risk appetite for feeder cattle was historically strong in 2014 – cattle feeders bet on the come through the entire year. And despite the sharp correction in 2015, the feeder market remained on a very similar course to 2014.

Looking at 2016, following steep feedyard losses in 2015, one would expect some pattern shift with respect to the deferred fed market – rotating back to a relationship that looks more like 2005-to-2013. But that hasn’t happened thus far in 2016. In fact, the pattern is remarkably similar to 2014 and 2015.

Switching gears: volatile markets have made strategic decision-making increasingly important in recent years. To that end, a recent column in Investment News titled, “Don’t Let A Good Story Replace Facts and Data,” caught my attention. Investment adviser Carl Richards, writing to others advisers, asks, “How do we help clients separate fact from fiction?”

He explains, “…we all know what happens when investors rely on anecdotes...There will always be people with a good story to tell about amazing investments. There will always be people who believe that personal stories trump the data and evidence saying otherwise. Our job as trusted advisers is to help our clients understand the true risk of relying on someone else’s opinion to justify big financial decisions.”

Greater data and evidence increases the chance of making a good decision. Coffee shop anecdotes simply aren’t reliable, and even if true, rarely repeatable. Producers need to be well positioned from a risk management perspective that includes consideration around all facets of the business.

As noted above, decision making is extremely challenging in this business environment. There are any number of external factors that are hard to navigate, including the market. Then there’s a whole separate layer to consider involving the operation’s financial situation and risk profile.

With that in mind, producers are encouraged to relentlessly review priorities within their operations while also investing time and effort in keeping up with both the market and the business environment in general.

Nevil Speer is based in Bowling Green, Ky., and serves as vice president of U.S. operations for AgriClear, Inc. – a wholly-owned subsidiary of TMX Group Limited. The views and opinions of the author expressed herein do not necessarily state or reflect those of the TMX Group Limited and Natural Gas Exchange Inc.

You might also like:

When is the best time to wean? It might be younger than you think

60 stunning photos that showcase ranch work ethics

Are you cutting hay? 10 new mower conditioners in 2016

3 key production areas that contribute to ranch-level sustainability

You May Also Like

Enter a zip code to see the weather conditions for a different location.