Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

After still another record-setting month, the cattle market appears poised to take a breather. After all, there’s a limit to how far packers will chase. However, this market continues to provide enduring surprises to the upside.

November 6, 2014

Fed cattle market action is generally pretty quiet in October. During the past 10 years, the monthly jump from the September high to the October high averaged only $1.00/cwt. – ranging from -$2.31 to +$3.29/cwt., excluding 2013. Last year, though, was a different story. The market jumped $6.43/cwt. and into the $130+ territory for the first time.

Not surprisingly (nothing about 2014 should surprise us anymore), this year’s October trade followed last year’s pattern and provided sharply higher prices. Fed cattle surged as the fourth quarter got underway. Once again, the market witnessed new all-time highs – a recurring theme that’s endured throughout the year.

During the front half of the month, buyers and sellers seemed content to settle into the longer-term pattern, with cattle trading within a $160-165 trading range. Meanwhile, the Choice cutout was trading around $250, forcing packers to operate deep in the red. As such, better trade from there appeared to be a long shot until wholesale prices gained some traction.

But as mentioned earlier, this year’s market has been full of unexpected twists and turns (favorably for sellers, those have all been to the upside). Despite higher retail prices, beef demand remains solid (see this week’s Industry At A Glance). And so even amidst negative margins, packers chased cattle to match customer needs and were especially competitive during the last half of October. Feedyards managed to leverage that reality and forced some sales as high as $170 (all the while the Choice cutout remained stuck at $249).

All that discussion brings us to the outlook going forward. Higher prices were easy to obtain while margins were working in the packer’s favor several months ago. And as noted last month, “…$160+ trade has now been tested several times; the question remains as to whether fed prices can break through overhead resistance and make a run at $165 or $170 going forward.”

Subscribe now to Cow-Calf Weekly to get the latest industry research and information in your inbox every Friday!

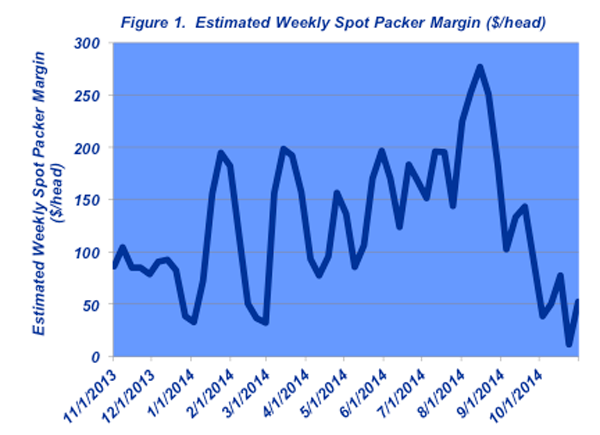

So while cattle made that stab at better prices, the wholesale market is seemingly struggling to advance. That’s created some very challenging margins in recent weeks. Choice cutout values peaked in early August around $260, while cattle traded at $160. Now cattle are trading closer to $168 with a $250 cutout.

That represents an $80 turnaround on the meat side and about $110-115 on the live side – in total equaling about a $190-200 margin reversal (Figure 1). Flirting with $170 in October put cattle about $5 above market expectations (based on a predictive model).

Given the challenging operating environment on the processing side, packers will likely work hard to claw back some margin in the coming weeks. Furthermore, the deferred futures contracts represent a flat pricing structure heading into the spring. As such, the market appears poised to take a breather here. There’s a limit to how far packers will chase; thus, gains may be more difficult to attain from here.

Therefore, it’s reasonable to expect fed prices to chop along through the end of the year. As alluded to earlier, though, this market continues to provide enduring surprises to the upside and has persistently rewarded cattle feeders to bet on the come. That’s the result of both enduringly solid domestic beef demand, but also favorable exports despite a strengthening dollar.

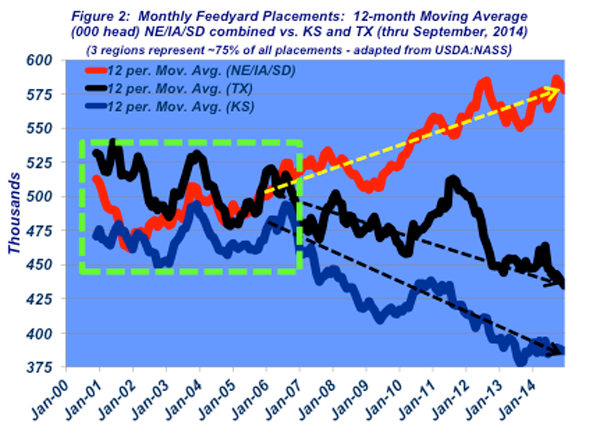

October’s Cattle on Feed report provided very few surprises or important signals to move the market. However, from a broader perspective the report revealed yet another month in which the regional variance in placements continues to be an important trend within the industry. The three-state region of Nebraska, Iowa and South Dakota continues to pull a greater portion of monthly placements vs. Texas and Kansas, respectively (Figure 2).

There’s any number of factors that have contributed to an increasing proportion of the nation’s fed cattle supply moving north over time. Chief among those considerations include the drought-induced cowherd liquidation in the South and the introduction of the renewable fuels (ethanol) mandate in 2005.

Corn prices in the Texas Triangle have spiked in 2014 vs. those in the northern feeding tier. That reality simply serves to accelerate the divergence between the north and south feeding tiers. Lower fuel prices will help moderate sharp basis trends. Nonetheless, the longer-run trend possesses important implications from both a fed cattle supply and feeder cattle basis perspective.

Noted at the start, fall generally tends to be a fairly tranquil period within the markets. Once the fall run is over, the industry seemingly bides its time through the holidays waiting on more active dynamics in the spring. That said, this market has been very challenging to predict and will likely be so going forward. There are a number of important influences that could bring even more surprises (both favorable and unfavorable) including:

Improving demand,

Cheaper fuel prices,

Post-election expectations and

Ongoing global uncertainties.

As noted during the past several months, “Trying to outguess or outsmart this market is about like trying to outrun a speeding train. It’s nearly impossible to do, and the consequences can be devastating.” Despite expectations for relative tranquility, ever-heightened levels of capital requirements point towards the need for strategic risk management. So, as always, it’s important to have objective information and disciplined review; both are essential to helping ensure successful decision-making going forward.

Nevil Speer serves as a private industry consultant. He is based in Bowling Green, KY, and can be reached at [email protected].

You might also like:

10 Utility Tractors For 2014 That Offer More Power & Comfort

Is The Cattle Market Nearing Its Top? Experts Weigh In

Why Freeze Branding Is ID Of Choice For Many Commercial Ranches

7 Of Our Nation's Best Stewardship Operations

Burke Teichert: Do You Want Progress Or Change In Cattle Breeding?

What Are Corn Stalk Bales Worth?

15 ATVs and UTVs That Are New For 2014

You May Also Like

Enter a zip code to see the weather conditions for a different location.

.png?width=300&auto=webp&quality=80&disable=upscale)