Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

From 1987 through 2006, I wrote and talked a lot about cattle cycles. My central theme was understanding cattle cycles and suggesting how cattle producers could make the cattle cycle work to their advantage.

Then, in 2006, ethanol production took off and pasture after pasture was plowed under and planted to corn. Add in the drought, and herd after herd was reduced or dispersed. Since then, the cattle cycle has, for all practical purposes, been broken. Beef cow numbers went lower every year and finally reached a several-decade low in 2014.

Today’s record beef cattle prices, coupled with rains in the Southern Plains, have triggered a renewed interest in expanding the national beef herd. Could this mean that the cattle cycle is alive again?

Let’s review a little cattle cycle history by studying a 2007 CattleFax chart (Figure 1) that I used over and over in past producer presentations. Figure 1 covers average cow-calf returns from CattleFax members from 1980 through 2007. The red bars represent the average of all participating member herds. I want you to particularly note the cyclical nature of cow-calf returns over this 27-year period by focusing on the red bars.

The yellow line represents high-return producers and the blue line represents low-return producers. Let’s first focus on the high-return producers — the yellow line. The cow-calf returns to these high-return producers followed the same cyclical patterns as the red bars — only just at a higher earned return level each year. Particularity note that for virtually all the years, the yellow line was above zero. Yes, the high-return producers tended to make a profit each year, both up the cycle and down the cycle.

Now note the blue line that represents the low-return cow-calf producers. The blue line also presents the same cyclical pattern, but with one major difference: For most of the years from 1980 through 2007, these low-return producers were below the zero line.

My conclusions from Figure 1 are:

• Cow-calf returns tend to be cyclical in nature.

• Every year through the good and bad years, there is a wide variation from one ranch to another.

• In the 2003 through 2007 time period, all three producer groups — average return, high return and low return — participated in the good times. We are in similar good times right now.

• Something is causing the cyclical nature of cow-calf returns.

Let’s turn to Figure 2 to get a partial answer as to why cow-calf returns are cyclical. Figure 2 presents the long-run USDA All Cattle Inventory Numbers for 1930 through 2004. Each big arrow on the chart signifies a cattle cycle.

We had a cattle cycle in the ’30s, the ’40s and the ’50s. We sort of had a cycle in the ’60s, and then we had a cycle in the ’70s. We peaked at 132 million head of cattle in the mid-1970s.

Some observations from Figure 2 are:

• Each cattle cycle peaked at a level higher than the previous cycle.

• A typical cattle cycle lasted from nine to 11 years.

• Cattle numbers started out each decade low, rose through the middle of the decade, and then turned downward.

• The downward trend went to the end of the decade, only to start the next decade’s cattle cycle.

We had another cattle cycle in the ’80s and again in the ’90s, but something was different. Cattle numbers did not peak above the previous decade’s cyclical top. The trend in cattle numbers after 1995 was downward and ended around 2004 — the longest cycle on record. After a slight increase in cattle numbers during 2005 and 2006, ethanol expansion and the 2006 drought together caused cattle numbers to continue downward through 2013 into 2014 — the longest decrease in cattle numbers in history. Starting in 2006, the cattle cycle was clearly broken.

We can summarize a typical cattle cycle by noting that we build beef cow numbers for approximately five years, and then we decrease beef cow numbers for approximately five years. The biology of the cow controls the speed of the expansion phase, while the magnitude of decreasing cattle prices controls the speed of the contraction phase. It is important to note that we can reduce cattle numbers faster than we can build cattle numbers.

So guess what? Now that prices are record-high, almost everyone wants to expand — at least that is what my phone calls suggest.

The Food and Policy Research Institute (FAPRI) at the University of Missouri publishes an annual agricultural outlook study listing its long-run projections for production agriculture. Figure 4 presents FAPRI’s March 2015 projected beef cow numbers through the next expansion into the year 2024. It is interesting to note that it has the next five years with a beef cow herd expansion, and years six through 10 with beef cow contraction. It is also interesting to note that it does not have beef cow numbers in the next cycle peaking above the 2010 level. Could it be that today’s 1,400-pound-plus slaughter animals have something to do with this? I suspect so.

The problem with the projected cattle cycles is that “cattle cycles cause beef price cycles.” It is the roller coaster effect of beef price cycles that ranchers find hard to contend with. Let’s take a look at historical beef price cycles.

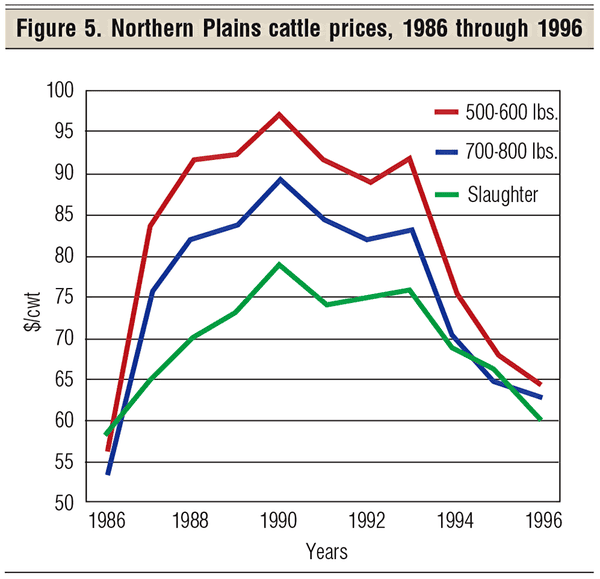

Figure 5 illustrates a typical beef price cycle for Northern Plains cattle, from 1985 through 1996. The red line represents 500- to 600-pound steer calf prices, the blue line represents 700- to 800-pound feeder steer prices, and the green line represents slaughter steer prices. Notice how much more calf prices and 700- to 800-pound feeder cattle prices rose and fell compared with slaughter cattle prices.

The distance between the lines represents the buy-sell margins for feeder cattle and slaughter cattle at any one time. The larger the buy-sell margin, the harder it is make a profit with retained ownership of calves.

Naturally, beef cow profits tend to follow the cyclical calf prices. Space, however, does not allow me to review the history of beef cow profits at this time.

Now you know what a typical cattle cycle looks like and something about the related beef price cycle. If the cattle cycle is indeed back as I am suggesting, what do you think beef cow profits will be during the rest of this decade? As you contemplate this, remember the biology of the cow limits how fast we can expand the herd.

FAPRI projects U.S. beef cow numbers up 7.5% by 2018 to around 31.2 million, from 29 million head in 2014. In turn, FAPRI projects 600- to 650-pound feeder steer prices will be 27% lower by 2018, compared with 2014. Next month’s Market Adviser will present my long-run price projections, heavily influenced by this historical review of cattle cycles. Stay tuned.

Harlan Hughes is a North Dakota State University professor emeritus. He lives in Kuna, Idaho. Reach him at 701-238-9607 or [email protected].

You might also like:

Is preconditioning still a no-brainer?

Burke Teichert shares the secrets of a profitable cow

Record carcass weights strain market weakness

How low-stress handling during weaning pays big

You May Also Like

Enter a zip code to see the weather conditions for a different location.

.png?width=300&auto=webp&quality=80&disable=upscale)