Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

Working for nothing is not reflective of a successful business.

April 17, 2014

Sustainability is a buzzword these days, often invoked by food-service providers and retailers who increasingly say they’re committed to sourcing food from sustainable beef production systems. Most sustainability definitions note the necessity of an economic or financial component, but the challenge of measuring financial and economic sustainability at the ranch level isn’t effectively communicated.

The necessity of having data to determine if changes in ranch production and marketing systems are economically viable is seldom mentioned. Thus, changes can be proposed without economic evaluation of their profitability. Many changes are cost-effective, but lack the numbers to show their profitability.

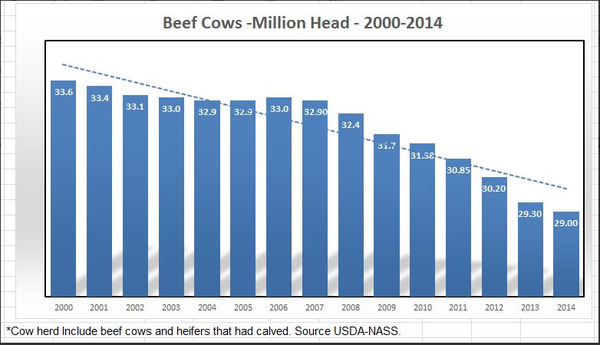

It’s clear that if a ranch’s production system isn’t profitable, production will cease, as there’s no economic incentive to maintain, invest or grow the business. And the continued decline in the national beef cowherd reflects an industry that is not being sustained. Thus, the profitability of change will be an important determinant if this trend is reversed.

The Internal Revenue Service (IRS) Schedule F, Profit or Loss From Farming, is the primary source of rancher financial reporting. It’s likely that more than 95% of beef cattle producers use cash accounting to comply with IRS rules.

Sign up now for BEEF Daily and get all the latest hot topics straight to your inbox!

But Schedule F doesn’t measure the profitability of the business or economic sustainability. And, often, inventory change, prepaid expenses, receivable or payables mean that cash reporting doesn’t measure profitability, either.

Following IRS rules for depreciation expense can create distortions. Producers should calculate depreciation using replacement cost, with reasonable useful lives and salvage values to measure profitability. Replacements should not be expensed.

Nor is there compensation for owner-operator labor and management in Schedule F. Working for nothing is not reflective of a successful business.

Every other major participant in the beef supply chain above the ranch level uses Generally Accepted Accounting Principles (GAAP) for financial reporting that measure profitability. These margin segments know their costs and profit margins.

Cattle Fax™ and others publish numbers on cow-calf cash profit. Cash profit is not even a valid financial performance term. Profit is what remains after all expenses are accounted for. Cattle Fax™ leaves out depreciation and returns to owner-operator labor and management. These are major costs at the cow-calf level and are completely inconsistent with the GAAP accounting that is used by others in the supply chain. Cattle Fax™ cash profit cannot be used to calculate business return on assets (ROA) or return on equity (ROE), which are fundamental measures of financial performance.

The methodology to measure financial or economic sustainability certainly needs to do more than use the IRS Schedule F cash-based reported “profit or loss” to define profitability. This was addressed in the Standardized Performance Analysis (SPA) methodology adopted by the National Cattlemen’s Association (NCA) in 1991 (see reference list). The accounting methodology used in SPA followed the Farm Financial Standards Council (FFSC) Guidelines. These methodologies use an accrual adjusted incomes measures of profitability.

Suggested definitions of profitability and economic sustainability are as follows:

• Financial profitability is measured by calculating the accrual adjusted revenue and expenses reported in the business accrual financial or profit or loss (P&L) statement. Interest is the cash and accrual interest paid. Raised feed is valued at cost of production. Breeding stock replacement cost is calculated using either the GAAP full cost absorption or the FFSC base value methods. Hired labor and management compensation equivalence is used for owner-operator compensation. Financial profitability is for a fiscal year and does not include real estate appreciation.

• Economic profitability is measured with the same financial accrual adjusted information with the additional adjustments of an opportunity cost for land (cash lease minus property tax and maintenance cost covered in a cash lease), raised feed at market value, and operating capital valued at opportunity cost. The opportunity cost of capital is a return expected on the next most profitable return on investment with similar risk. Economic profitability is a measure of the consequence of entry or exit of the business.

The best measure of sustainability is economic profitability because individual business financial sustainability is heavily influenced by the owner equity and repayment capacity position. For published comparative evaluation of ranch, systems or practice purpose, profit measures are pre-income tax and do not include appreciation of land. Of course, the rancher should use both measures of performance as done in SPA.

With the volatility in commodity prices and production cost, a sustainable business does not have to be profitable every year. A lender would like to see financial profitable performance for the past three years, and a business plan that can demonstrate cash flow and profit potential for five years. It’s not often they get this information. The business debt situation and repayment capacity are critical considerations for an ongoing or sustainable business.

By a business definition, the cow-calf sector is not being sustained. The sector has the smallest beef cow herd since 1941. It’s going to be a challenge to measure an “economically sustainable” price level for cow-calf producers and impacts of alternative production and marketing systems that change environmental, social and consumer desired dimensions of sustainability. The reporting and communications burden is on the ranch sector because other beef businesses in the supply chain already have their reported standardized measures of profitability in place. And others in the supply chain will not take the responsibility to measure ranch economic sustainability of the changes they wish to impose on producers.

References:

• National Cattlemen's Beef Association National Integrated Resource Management Coordinating Committee, Cow-Calf Financial Analysis Subcommittee. NCA-IRM-Standardized Performance Analysis (NCA-IRM-SPA): “Guidelines for Production and Financial Performance Analysis for the Cow-Calf Producer: Cow-Calf SPA.”

• Texas Agricultural Extension Service, Texas A&M University (TAMU) Department of Agricultural Economics, Aug. 15, 1991. For Cow-calf SPA information, go to http://agrisk.tamu.edu. Stan Bevers manages the SPA information, software and database.

• Farm Financial Standards Task Force. “Recommendations of the Farm Financial Standards Task Force: Financial Guidelines for Agricultural Producers.” Revised 2008, Farm Financial Standards Council – www.ffsc.org.

James McGrann is a former Texas A&M University professor and Extension economist. He is regarded as the “godfather of standardized performance analysis (SPA),” a program that helps ranch managers analyze production and financial data by comparing it to benchmark data. McGrann was also among 50 U.S. beef industry figures lauded in September 2013 for their notable contributions of the past half-century.

You Might Also Like:

Can The Beef Industry Get Along?

Skipping The Basics Can Carry A Big Bottom-Line Penalty

Will Crossing Two Clones From Prime, YG1 Carcasses Produce Similar Offspring?

80+ Photos Of Our Favorite Calves & Cowboys

You May Also Like

Enter a zip code to see the weather conditions for a different location.

.png?width=300&auto=webp&quality=80&disable=upscale)