Subscribe to Our Newsletters

BEEF Magazine is the source for beef production, management and market news.

Supply is the story that just doesn’t go away. And, if anything, it will be exacerbated in 2013, starting with the cowherd.

January 2, 2013

If you know poker, you know how complex it can be when all players remain in the game after several rounds of betting. The game gets particularly challenging, with wide open combinations of both cards and player strategies. Those circumstances make decisions tough and unpredictable.

The beef complex starts out 2013 in a similar environment. Lots of influences and sources of turbulence stubbornly remain; these include factors such as economic policy wrangling, ongoing concern about drought prospects and continuation of ever-tightening cattle supply, as well as many others.

Before moving into 2013, though, let’s first step back and look at the markets from a broader perspective. Figure 1 highlights the 52-week moving average for the Choice cutout and the fed market. Both moving averages finished 2012 at all-time highs: about $191 and $123 for the cutout and live market, respectively. The graph also underscores the importance of consumer spending and its influence on the wholesale market – as the cutout goes, so goes the live market.

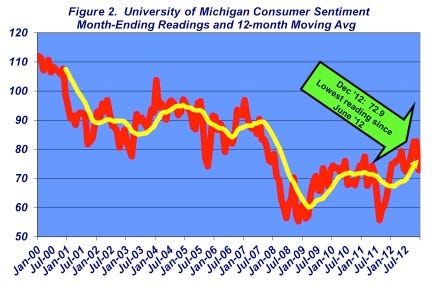

That brings us to the state of the consumer for the coming year. Beef demand through 2012 has remained surprisingly solid despite relatively tepid consumer sentiment (Figure 2) and general cautiousness around the broader economy. That’s facilitated the ability to pass on higher prices through most marketing channels.

However, that capacity will reach some upper limit. To that point, Fitch Ratings 2013 outlook for commodity protein, produce and dairy explains that:

"…consumer price fatigue remains a risk for the protein industry, given that CPI for proteins has outpaced increases in the broader food-at-home CPI since 2010…Fitch believes chicken processors have the best pricing power given a positive longer term outlook for consumption and lower relative pricing. For example, for the year-to-date period ended October 2012, the average U.S. retail price of chicken was $1.88/lb. vs. $3.54/lb. for pork chops, and $6.23/lb. for beef steaks.”

Will consumers begin to hold back their beef spending? That remains to be seen, but that very consideration mandates careful monitoring around general consumer attitudes regarding the economy and policy.

Turning our attention to the production side, both the fed and feeder cattle markets have found some renewed support at the CME. April live cattle have resurged during December with the contract establishing a new lifetime high at $138/cwt. Meanwhile, the spring feeder cattle contracts have followed accordingly and flirted with $157-8/cwt. The strength is being driven by hopes for solid demand and ever-tightening supply throughout the beef complex.

Supply is THE story that just doesn’t go away. And, if anything, it will be exacerbated in 2013, starting with the cowherd. The cow marketing rate is always very telling regarding year-to-year intentions among cow-calf producers. It reflects their relative ability, and risk appetite, to retain vs. market cows. In aggregate, that spells either expansion or contraction.

Figure 3 depicts that reality. Since the mid-'90s, the cow marketing rate serves as a fairly reliable predictor for the following year’s cow inventory. An annual cow marketing rate of approximately 8% would equate to a steady number of cows (lower rates equal expansion, higher rates reflect reduction). The marketing rate in 2012 should be approximately 11%: that equates to an approximate decline of 2% for 2013’s starting cow inventory (or about 29.3 million cows in 2013 – down from 29.9 million head in 2012). Therefore, there’ll likely be continued shifts in business strategy all around the protein complex (See "Industry At A Glance: Out-Front Beef Sales Increasing.").

Canada, Mexico feeders dwindling

That’s compounded even further by the likelihood of dwindling feeder cattle imports from Canada and Mexico in 2013. With respect to the feeder market, all things will turn on weather and grass availability in the coming months. Strong fall futures and grass fever (if there’s some spring rain) will prove especially supportive to the calf market. And if that occurs, there may be an even bigger bite out of supply with the possibility for increased heifer retention. Conversely, another dry year could prove very disruptive to the feeder cattle market from the standpoint of grass availability, subsequent early bunching of feedyard placements and tight corn inventory.

A Closer Look: Border Imports Portend Tighter Feeder Cattle Supplies

Considering the hectic business conditions in 2012, one would like to think it might get easier in 2013. No such luck – there are still lots of external factors that must be sorted through on an ongoing basis (we haven’t touched on the international markets – another discussion for another day). So for now, look for continuation of some busy days ahead.

Whatever your role in the value chain, daily challenges around the business are compounded by the ongoing escalation of capital-at-risk. Therefore, mentioned every month as an important reminder, there’s always the need to remain informed and maintain objectivity around all aspects of the business. With that in mind, Benjamin Graham provides some enduring advice that holds true for any owner/manager making important business decisions (The Intelligent Investor, c. 2003): “Have the courage of your knowledge and experience. If you have formed a conclusion from the facts and if you know your judgment is sound, act on it – even though others may hesitate or differ.”

You May Also Like

Current Conditions for

70°F

Partly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.

.png?width=300&auto=webp&quality=80&disable=upscale)